(Bloomberg) — An insurance product that consumers use to help fund their retirements is selling at record levels, powering demand for corporate debt and commercial mortgage bonds.

Most Read from Bloomberg

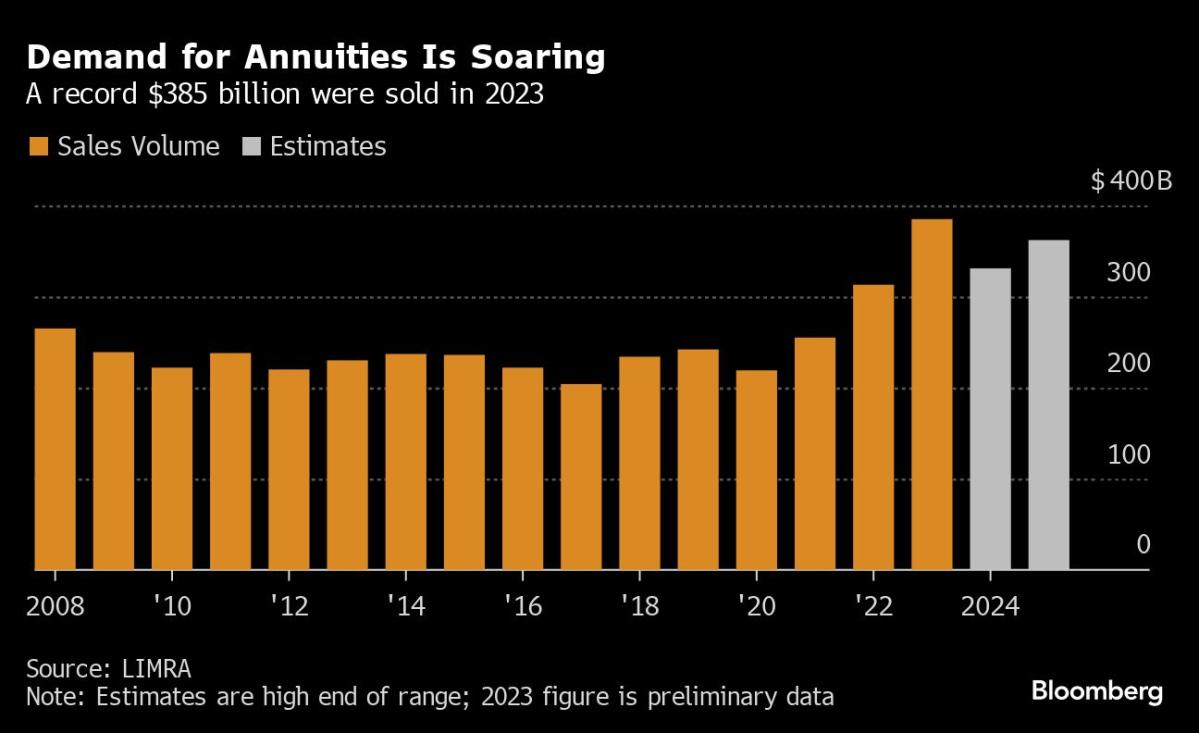

Last year, sales of annuities, which allow consumers to effectively buy income for the rest of their lives, reached an all-time record high of $385 billion, according to life insurance trade group Limra. That’s up 23% from the year before. The products grew more attractive as rising interest rates translate into higher potential annual payouts from the products.

Behind the scenes, the life insurers that usually sell annuities are buying bonds to generate income for the products, and in particular, corporate debt and asset-backed securities including mortgage bonds. Their demand might decline a bit this year after bond yields have fallen, but Limra says annuity sales are still expected to remain strong by historic standards.

The insurers’ bond purchases underscore how demand for many debt securities now is driven by demographics, and illustrates why valuations for corporate bonds can remain high even as the Federal Reserve keeps monetary policy relatively tight.

“Key drivers for credit demand at the moment are retail and pensions seeking higher all-in yields, and annuity sales driven by more baby boomers retiring and by a higher level of interest rates giving policyholders higher monthly payments,” said Torsten Slok, chief economist at Apollo Global Management.

Money raised by annuities often goes toward investment-grade debt, usually fixed-rate and ranging between three to 10 years — broadly in line with annuity durations, said Deutsche Bank AG strategist Ed Reardon.

For investment-grade corporate bonds, demand from annuities and other investors catering to retirees are helping to keep valuations high. The average risk premium, or spread, on a company note rated BBB- or higher is 0.95 percentage point, close to the tightest level in the last two years.

Over the last two decades, spreads have averaged closer to 1.49 percentage point, according to Bloomberg index data.

Record inflows into fixed-rate annuities are also a strong driver of insurance demand for commercial mortgage-backed securities, Reardon wrote in a Feb. 6 note. AAA CMBS excess returns in 2024 are higher than those of both investment-grade and high-yield corporate debt, according to Reardon.

The average AAA CMBS spread versus Treasuries stood at 0.88 percentage point as of Friday, having fallen roughly 30 basis points from an October high, data compiled by Bloomberg shows.

Over the next two years, annuity sales could total as much as $693 billion, according to estimates from Limra. The group expects sales of up to $331 billion this year — a decline from 2023, but a level that would still have been a record in 2022.

“Last two years has been going gangbusters and the expectation is for this year to be the same,” said Dec Mullarkey, a managing director overseeing investment strategy and asset allocation at SLC Management, which manages $264 billion. Falling rates “will impact demand somewhat,” he cautioned, “but they will still be at reasonable levels, that all-in yield will still be attractive versus history.”

Fixed-rate Deferred Annuities

One type of annuity that is selling particularly well are fixed-rate deferred annuities. Policyholders make an investment upfront, which accumulates interest at a fixed rate over a set amount of time. After the so-called annuitization point, they can start receiving income payments.

The product line recently had its best-ever quarterly sales, with $58.5 billion sold in the fourth quarter, up 52% from the year-ago period, according to Limra. Volume totaled $164.9 billion in 2023, up 46% from the 2022 annual high of $113 billion.

Annuities tend to be most popular among people nearing retirement or who have already left the workforce. The average age for those buying the products is around 62, according to Bryan Hodgens, head of Limra research.

Roughly 17% of the US population was over 65 years old in 2022, compared with about 12% in 2000, data from the Federal Reserve Bank of St. Louis shows.

Any rate cuts by the Fed this year would also buoy corporate debt as prices rise when yields fall.

“Credit has consistently outperformed other sectors of fixed income since mid-2020, and the surge in annuity sales is almost certainly part of the reason,” wrote Steven Abrahams, head of investment strategy at Santander US Capital Markets, in a note. “That is a positive for credit performance going forward.”

(Updates Elsewhere in Credit box. A previous version of the story corrected the y-axis label in the second chart.)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.